Quarterly INsync Chit Chat April 2026

QUARTERLY “INsync” CHIT CHAT

April, 2026

Contrarian Skiing [by David Cox]

My two youngest kids and I, Emry (15) and Eloise (11) got away for a few days over March break and we started our journey at the Splash Lagoon Park in Erie, PA for some good ‘ole fashioned waterslides, tube-rides (and yes some lazy river floating in there too). From there, we went to Ellicottville, NY for some skiing and the first day was 14 degrees C! VERY spring-like but the snow was in surprisingly welcoming conditions and fun was had by all. Eloise had never been skiing where there were six lifts and that much terrain (even though half the place was closed) and we heard that over 50% of reservations had been cancelled (surely due to the warm weather) which meant it was our personal ski hill. That afternoon temperatures dropped and we got 20cm+ of snow for a seriously awesome powder day #2 and never waited in a single line up the whole time! So much fun!!

Meet Miss Bella! Our newest addition and to say she’s loved is an understatement! While her first day with us as we drove home from the Perth Humane Society didn’t exactly go as well as I would have hoped (the poor little kitty was sick to her stomach!) – she’s settled in really well! The kids absolutely adore her (and me too!) and she loves to play, chase balls, hop up on the counters, meow sweetly for more wet food and find new spots to lay down, relax and peek out of the windows. After first having a cat many years ago in Vancouver, our Bella is a sweet new resident and part of the family!

News – Some That You’ve Heard, Most That You Haven’t - [by David Cox]

Air Canada CEO quits over furor over crash condolence video. U.S. fuel prices soar as Trump reportedly weighs war exit. U.S. executive order requiring contractors to certify they won’t do “racially discriminatory DEI activities”, or risk contract cancellation. Conference Board of Canada’s “Leaky Bucket” study shows 1 in 5 skilled immigrants leaving Canada within 25 years, set to hammer tax revenues, while politicians fight culture and trade wars. Toronto approves municipally run grocery stores to offer cheaper food in a 21-3 vote by councillors. Canada posts the weakest GDP per capita growth over 10 years at 0.5% (weaker than even Germany +4.7%) showing a lost decade. Bloomberg: Markets see the Bank of Canada hiking interest rates more aggressively this year amid surging oil prices and hawkish messaging from peer central banks.

Book Corner [by David Cox]

I’ve always loved the math of the game of pool: the geometry, the angles and visualizing the cue ball hitting the object ball for a perfect roll into the pocket. But there are so many common ways to sewer the cue ball and get ourselves stuck when trying to make a run on the balls.

After my team won both our 8-ball & 9-ball leagues in the fall, it’s time to sharpen up my game for our upcoming regional finals that will determine who goes to Las Vegas to play in the World Pool Championships. A skilled player or two has encouraged me to cultivate my natural skill (whatever I have is from my parents’ basement growing up) and I’ve upped by game with a break cue and a new Predator Sneaky Pete playing cue to take advantage of today’s technology.

I also visited the Amazon reviews and found this book by Phil Capelle which has been an awesome read! With countless table graphics, analysis of common situations (both offensive & defensive) and deeper insights into not only how to make our shots more successful, but of course, how to leave the cue ball in a way that leaves us a high probability shot right after the last. I will highly recommend this book if you’re looking to better your game!

Wellness Wins! - [by Avery Kelly]

As we jump into the spring season, I hope each and every one of you has had the chance to take some time for YOU! As we discussed last quarter, weaving even one hour of stress reducing activities into your weekly routine can make all the difference when it comes to your health. This quarter I wanted to discuss the benefits of strength training. For many, strength training can be seen as super intimidating, however research shows that as we age, any muscle mass we do not continue to use, we will lose.

Strength training in no way means squatting 350lbs or bench pressing 225lbs, but rather using resistance bands, bodyweight exercises, or anything that requires your muscles to lift a heavy object against gravity. Even the smallest of activities, a part of your daily routine can make a big difference. Whether it is walking with wrist weights on, participating in a group fitness class, or even pumping some iron – strength training will positively impact your physical function as you continue to age and face other mobility limitations.

I personally have been enjoying group strength classes. These allow me to schedule intentional time into my day, listen to great music, and feel constantly motivated by those around me. Let us know if you try out some strength training!

What Are We Buying? Selling? Holding… [by David Cox]

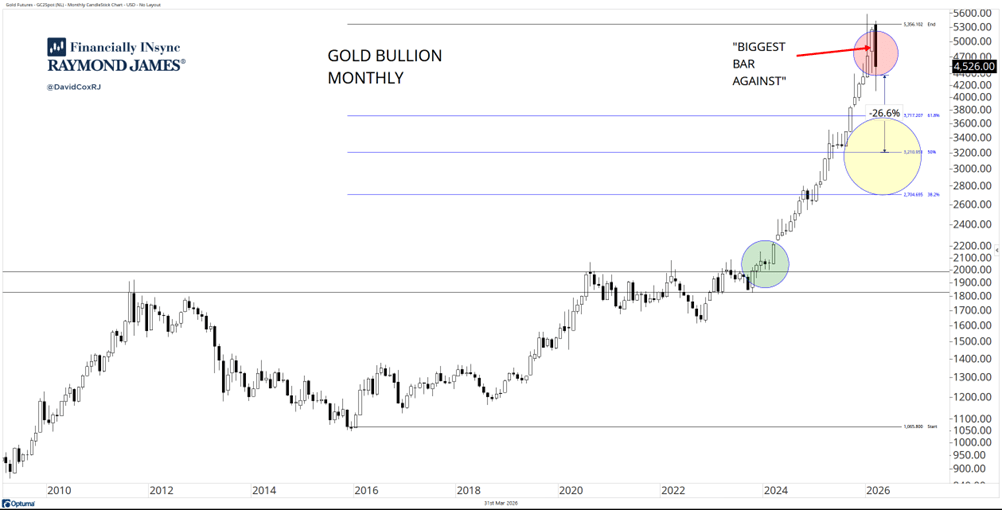

We’ve owned gold in our portfolios for the past several years and the low correlation and stronger upside (in hindsight!) made it a helpful contributor to portfolio gains. As gold prices have risen, the narratives related to debt concerns, de-dollarization and the diversification away from holding U.S. debt as an asset have all fueled increased demand and when faced with a limited supply of sellers, prices rise. But, like all prices, corrections and counter-trend moves can and do occur against the primary trend.

On a big picture basis, gold remains in an uptrend, but the recent price activity since late January to me looks like distribution and leads me to conclude that gold just peaked. Before jumping to conclusions, am I saying that gold has to fall all the way down to the level of years ago and erase all the gains that have been? No! But when gold really broke out in early 2024 and moved above the $2,000 USD level, it went up significantly rising to more than $5,500 in just more than two years. It has since fallen almost $1,000 from those highs and is set to finish the month of March with the “biggest bar against” and a bearish engulfing candlestick.

For those less technical, it means that prices had risen without encountering excess supply but that has changed as sellers became more aggressive and a peak formed this winter. Do I believe gold will go higher in the years ahead? Yes, for sure I do. But will I be surprised if we consolidate and even move back down to the $3,000s? Nope. All things are possible.

But I do know how to spot a top and while I’ll admit that I never know if it is a big, important top, or just a short-term top, it starts somewhere. Our clients take risk off at tops, not knowing if a short-term top becomes an intermediate-term top, which can become a long-term top. We’ve sold our gold & silver bullion positions in #AllINsync this past quarter, which represented as much as ~15% or so of the portfolio at times in the past year. I’ll have no qualms or second thoughts about reacquiring gold if the technical conditions support the idea.

Also worth mentioning is that we still have lots of clients that hold gold (have for years) and will likely continue to do so, to defer the taxes due on the capital gains and continue to focus on the longer-term protection of their wealth. And I too, hold physical gold and silver and have made no adjustments to my holdings despite the price action, taking a long-term stance vs. a tactical investment related one. Please don’t hesitate to ask us questions if you’d like more clarification in this area.

Source: Optuma

* as at March 30th, 2026

Things We Recommend - [by Avery Kelly]

This past year, I have been a frequent user of the app Beli. This application allows you to bookmark restaurants you are interested in visiting, rank the spots you’ve already tried, and even see your friends’ thoughts on new ones!

What I enjoy about this application is that it doesn’t require you to simply rate the restaurant or café out of 10 – instead you are asked to compare it against other spots you have tried. This means that as you try new restaurants, a spot that was previously ranked 2nd could move up or down on your list.

As you continue to rate new spots, you will be given a “taste profile” which helps to provide tailored recommendations and even compares you friends’ preferences to your own.

My favorite part: the Beli app can be used all over the world! I am happy to say I have currently ranked over 85+ spots across all of North America and have even used this tool to help decide on restaurants in Europe (and for David in Dubai!).

Artificial Intelligence -> Human Wisdom? [by David Cox]

I find myself so regularly scheming about what I can ask AI for next. This past month, I fed it our short put option positions including tickers, strikes and expiries and asked for it to help me design a process to better adjust the positions as market conditions deteriorate and as volatility rises. A new set of rules appeared, and while almost nothing I take from AI is deemed worthy without further analysis (myself), I have to admit the rules were disciplined and in character of how I typically face portfolio management decisions with a desire to act unemotionally and prudently as things change.

What issue are you facing these days? Prompting AI is so easy to do and really doesn’t take any know how, in fact, it seems that the worst case scenario means it will lead to you thinking in some different ways, perhaps on different angles and might even just solve that issue you’ve been having around the house or…

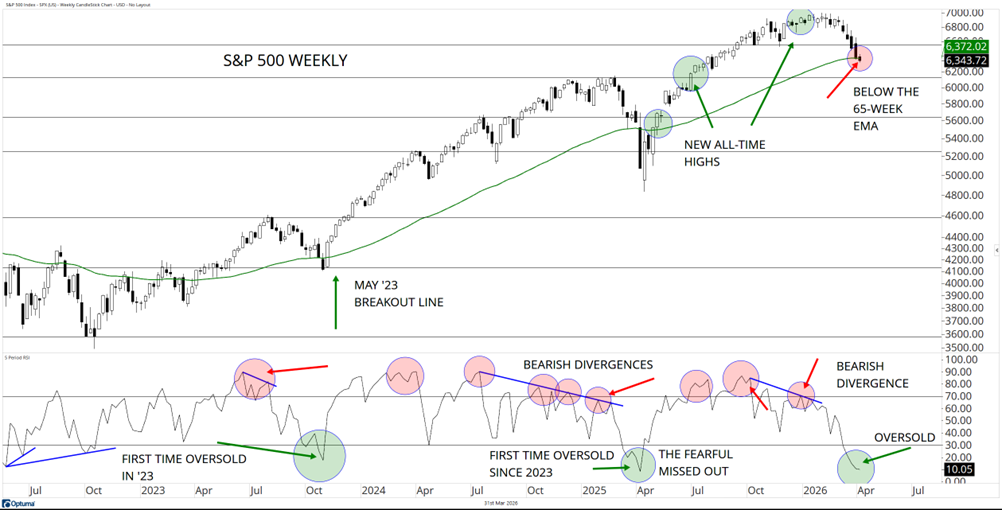

How’s the (Bigger Picture) Market? [by David Cox]

As always, we use the S&P 500 (U.S. stocks) as our barometer of risk-taking as investors. Why is that again? Don’t some of us live in Canada, or elsewhere in the world? The U.S. market is huge by comparison (to every other market!) and has approximately $69 trillion USD worth of market capitalization vs. Canada at roughly $3.4-4 trillion. A single mega-cap like Nvidia (~$4 trillion) dwarfs the size of many stock markets themselves (oh Canada!). But, I digress.

For the first time since last year (remember the “Tariff Tantrum”?) or the so called “Liberation Day” period last spring? Markets fell swiftly and strongly and somewhat similarly have been falling this time around and are now sitting “oversold” (lower panel). This typically happens once a year, but this does not mean that we can buy with 100% certainty. Stock markets are volatile and can be subject to corrections, selloffs and/or bear markets, which can take place through price or time. We haven’t had a protracted bear market since 2022, is it time? At this point, we have the S&P 500 sitting down against my big picture 65-week exponential moving average (green) and still have higher highs and higher lows, BUT, the monthly chart does show some wear and tear and some considerable selling which at this juncture looks a little more heavy than it did last year. Add to that the passage of time (the bull market is in its fourth year) and you find me being more cautious as we evaluate our current conditions.

To paraphrase Joe Friday, “all we want are the facts, ma’am”. And those facts will show up in the behaviour of investors, which leave their footprint via price. We’ll continue to monitor price carefully and adjust (as we always do) accordingly.

Source: Optuma

* as at March 30th, 2026

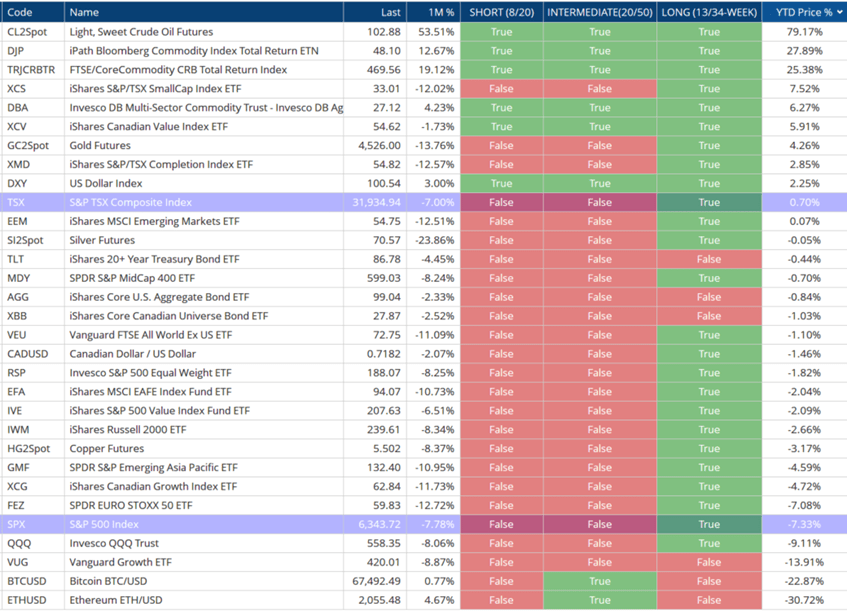

Market Summary and Trend of “All Assets” - [by David Cox]

Our “all asset” table, which is designed to be an overview containing assets from stocks to bonds to commodities and from east to west, shows our current environment well. We are in the midst of long-term uptrends (note the green/”true” in most cases), but have turned short and intermediate-term negative as markets have fallen, most recently since the Venezuela and then Iran war has begun.

I’ve highlighted both the Toronto stock market and the U.S. market and sorted by YTD % change, you can see that Toronto is still holding some gains (though barely!) of +0.7% vs. the S&P 500, which is -7.3% thus far in 2026. The strongest asset of course is crude oil, which has risen +79% this year (though remains below its 2022 highs ~$130/barrel and the 2008 highs ~$147/barrel). So for those of you thinking that gas prices are high (I saw $1.8/liter recently!), it’s possible we haven’t seen anything yet [I don’t want to rub in the fact that my electric vehicle charging costs have not changed one iota since oil surged upwards].

I do believe that we’re going to continue to see non-U.S. equities rise in relative importance in the coming years, though we must remind ourselves that relative strength is good, but it needs to be combined with absolute strength (i.e., losing less than a given market, is still losing). It’s been an impressive bull market since the bottom in October, 2022 and we must not be complacent about different scenarios moving forward.

Source: Optuma

* as at March 30th, 2026

The Narrative is Wrong - [by David Cox]

They keep telling us the same thing. Our governments’ and central bankers keep telling us that they’re going to bring interest rates down and know full well that the borrowing binge is a problem. Do we give an alcoholic another drink? Do we give a heroin junkie heroin (oh wait, in B.C., we do do that, bad example)… the Bank of Canada has dropped interest rates 7 times since September, 2024 and the U.S. Federal Reserve has dropped interest rates 6 times and yet in BOTH cases, actual rates (a.k.a. yields) are higher now than when those rate decreases started.

The bond markets are huge, and it’s the demand and supply that moves interest rates. I’ll continue to suggest (as I have for many years) that the market has woken up to the reality that not only is the borrowing unsustainable, but it’s actually far riskier than ever and as such, higher rates are being demanded by those willing to lend to the government.

Look at the most recent environment that we’ve had this past month since the U.S. and Israel started war with Iran. Interest rates have risen. And before that even started, commodities were rising and what do increases in commodity prices lead to? Inflation! And what do the central bankers have to do as inflation rises? Raise rates! Not drop them. The government is in a tough spot and ever since 2020 when they increased our money supplies to absurd levels (i.e., ~60+ in one year in Canada), they’ve pricked the bear and the game has changed.

Getting AllINsync [by Kieran O’Donnell]

Now that it is officially spring it’s time to do some spring cleaning – this time in the form of “future housekeeping” for your executor. Yes, I’m talking about estates and today we are reviewing the Executor, who they are, what they do, when they do it, where they are needed and why their role (and why the right one) is so important.

I’m sure you have all heard the term executor when referring to an estate and if you have not, let me break them down for you. An Executor is the party appointed in your will to administer your estate and carry out your final wishes. Their role begins immediately upon your passing, at which point they are responsible for gathering your assets, settling outstanding debts, filing necessary tax returns and ultimately distributing your estate to the intended beneficiaries. In fulfilling these duties, executors interact with a range of institutions – including banks, tax authorities, legal professionals and the probate courts – to ensure every requirement is met. Without a capable and clearly designated executor, the estate process can become delayed, disorganized and far more stressful for your loved ones.

Choosing the right executor is critical because failing to name an appropriate party – or not naming one at all – can create complications that extend far beyond paperwork. Without a designated executor, the courts must appoint an estate administrator, a process that can lead to delays, frozen accounts and uncertainty for loved ones. Even when someone is eventually appointed, the absence of a clear plan often fuels unnecessary family conflict at an already emotional time. Likewise, selecting the wrong executor can be just as problematic. An appointee who is unprepared and overwhelmed may struggle with deadlines, communication or financial responsibilities. Resulting in avoidable stress and potential legal issues. Ensuring the right person or professional is chosen helps protect your estate, minimize delays and provides clarity when it matters most.

One of the most practical ways to support your executor is by keeping an organized, up-to-date inventory of your financial and personal information. A comprehensive list of accounts, insurance policies, legal documents, passwords or digital access instructions, contact information for professionals and details about debts, subscriptions and recurring payments can significantly reduce stress and prevent delays. Much like seasonal spring cleaning, reviewing and refreshing these details regularly ensures your executor can quickly locate what they need and carry out your instructions with confidence.

While many people choose a family member or friend as executor, there is a growing trend towards choosing a corporate executor. A family executor may offer personal familiarity and little to no cost, but they may also face emotional strain, limited experience and/or potential conflicts. A corporate executor, via a trust company like Solus Trust here at Raymond James Ltd., provides neutrality and professional expertise. A lawyer can also act as executor, bringing legal knowledge and impartiality, but professional fees will also apply. Understanding these options allows you to appoint the party best positioned to manage your estate effectively.

Taking the time to choose the right executor and prepare them with organized information is one of the most meaningful ways to protect your estate and support your loved ones. As you refresh pother areas of your life this spring, consider reviewing your estate plans as well. A thoughtful, well-prepared approach today can make all the difference in the future.

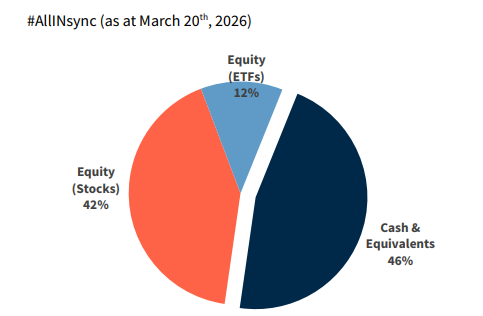

AllINsync: How Are We Exposed? [by David Cox]

As 2026 started off with a very strong January (déjà vu!?), we’re now facing a rapidly weakening investment environment as we close out March (déjà vu again?). While you’ll be forgiven for trying to choose the most recent narrative or news du jour to blame on the conditions, we should really understand that we’re always faced with something. Recent wars or political upheaval in Iran, or Venezuela really aren’t new, they’re actually status quo common as time goes by. But indeed, volatility tends to increase and fear rises as a correction takes hold, which tends to happen after a period of rising prices.

While our geographic positioning hasn’t changed much in the past quarter in #AllINsync, we’ve no doubt shifted more defensively in attempt to protect our profits and maintain our earlier gains. There is now a very stark contrast between U.S. equity returns and Canadian equity returns in the past year. In the 1-year from March 31st, 2025, the S&P/TSX +29.0% vs. S&P 500 (in C$) +10.8%!

As I write this (March 31st), our clearly growing cash pile is evidence of our approach to keep taking risk off as stops trigger, as the market declines and as uncertainy increases. We’ll be happy to redeploy this cash into the opportunities that are no doubt are being created by this selloff!

Source: Croesus

* as at March 30th, 2026

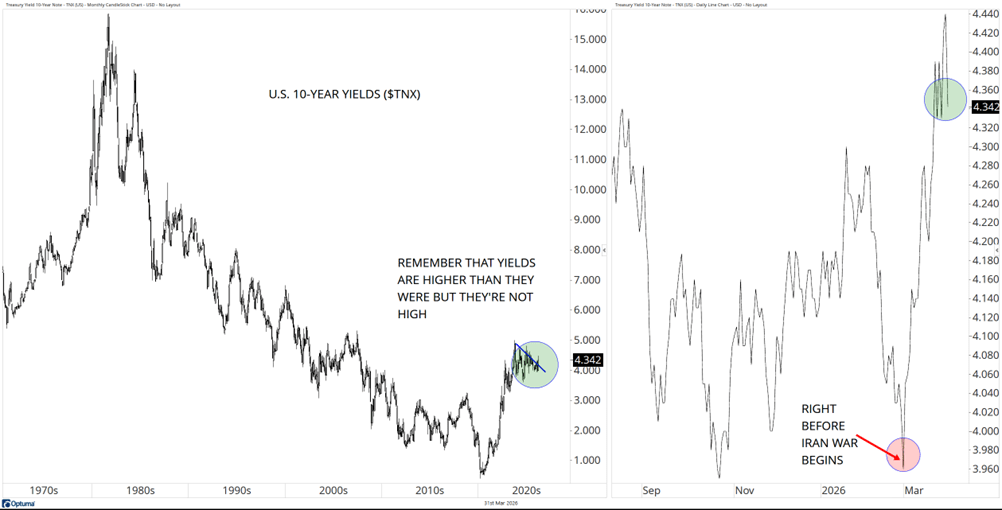

Chart of the Month - [by David Cox]

Remember the old days? When bonds rose and provided an offset to weaker equity returns? The days when the “60/40” portfolio was built to better withstand short-term fluctuations in volatile market conditions? That’s so yesterday.

Since the Iran war has started, 10-year yields have moved upwards, globally, and are serving to put the central banks on notice that their short-term manipulations aren’t sufficient to change the longer-term borrowing costs for their governments, companies and individuals. Sure, they can try to encourage borrowing at the short-rate, being held lower by the demands of those in power, but there is risk is not accepting that while interest rates are higher than they were six years ago (in 2020) without question, they’re not truly high.

Many of you remember the 1980s and the high cost of home mortgages, the seemingly generous rates on GICs/CDs and in those days, the interest that the banks paid us for trusting them with our money (those days are long gone!). On the chart below (left), we have the 60-year chart of U.S. 10-year yields ($TNX) and on the right side is the zoomed in version of past 7 months and you can see that we’ve gone from ~3.95% in late February to ~4.3% today as I write this. The media will tell us to blame Iran, or rising oil prices or Trump or Israel, but the reality is that in 2020 rates bottomed after declining for 40-years and a radical new environment was ushered in. Instead of complaining, let’s consider its implications on our investment portfolios, our financial assets and liabilities and adapt instead of pointing fingers.

Source: Optuma

* as at March 30th, 2026

Social Media and Our Website - [by David Cox]

Do you follow me on “X” (formerly Twitter)? I can be spotted @DavidCoxRJ and regularly post charts and market context if you’re interested! You might even spot our team on YouTube in 2026 as we potentially develop a channel focused on investment education and debunking investment myths that are pitched regularly by the media as gospel.

Here are a few recent posts that got some attention:

Upcoming Dates, Seminars, and Announcements - [by David Cox]

What: Guelph Village Media – “Leverage & Borrowing: Good Uses vs. Downright Irresponsible Uses”

Where: Guelph, ON

When: April 2nd, 2026

Who: I’ve been invited to speak to a local group of folks and talk about leverage!

What: “CNBC Arabia”

Where: www.cnbcarabia.com

When: April 8th, 2026

Who: I’ll be a guest on the show and no doubt talking about the state of the equity markets in the face of the U.S./Israel vs. Iran war.

What: “CMT Fill the Gap Podcast”

Where: https://cmtassociation.org/education/podcasts/

When: May 6th, 2026

Who: I’m very excited to join fellow CMT charterholders David Lundgren and Tyler Wood and have an opportunity to discuss my investment philosophy, decision-making tools and share lessons my own history book!

What: “CMT Proshares Education Event”

Where: TBD

When: May 13th, 2026

Who: I’ll be sharing the stage and providing investment insights and education as part of the conference.

I hope you found something in our Quarterly INsync Chit Chat that causes you to smile, or think, or perhaps consider as seek to move forward in what often seems to be such a crazy and uncertain world!

Sincerely,

David Cox, CFA, CMT, FMA, FCSI, BMath

Senior Portfolio Manager, Wealth Advisor

Raymond James Ltd.

Phone: 519.883.6031

Unit 1 – 595 Parkside Drive | Waterloo, ON | N2L 0C7

david.cox@raymondjames.ca

www.financiallyinsync.com  @DavidCoxRJ

@DavidCoxRJ

Disclaimer: Information in this article is from sources believed to be reliable, however, we cannot represent that it is accurate or complete. It is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell securities. The views are those of the author, Financially INsync Team, and not necessarily those of Raymond James Ltd. Investors considering any investment should consult with their Investment Advisor to ensure that it is suitable for the investor’s circumstances and risk tolerance before making any investment decision. Statistics, factual data and other information are from sources believed to be reliable but accuracy cannot be guaranteed. It is furnished on the basis and understanding that Raymond James Ltd. is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities. Raymond James Ltd. is a Member Canadian Investor Protection Fund. Raymond James (USA) Ltd. (RJLU) advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Raymond James (USA) Ltd., member FINRA/SIPC.