Quarterly Strategic Review - 1st Quarter (Jan-Mar, 2026)

With the seeming endless supply of concerning headlines and risks, I’d forgive the average person (not necessarily our clients though!) for getting caught up in what ultimately is noise. It’s noise that sells media spotlights, gets clicks online and yet gets in the way of making wise investment decisions and/or distracting us from otherwise reality.

Those of you that know me, know that I don’t like violence and I don’t care to see wars so regularly happening all over the place, bombs dropped without much thought and I tend to take a skeptical perspective on so much of what we hear (and see!) as I know it’s being told through the lens of government A or government B, who are trying to drum up support for cause C or cause D. Reality is often some mix of what we’re told and yet a narrative can become quite persistent. Let’s use a current example like oil prices. For those of you that drive gas-powered cars, you’ve obviously experienced a much higher cost to fill your tank in the past couple of months. But do you remember years ago when it was even higher? Oil prices aren’t even where they were at in 2022 (last U.S. president) and even less so where they were in 2008. Really you say? Yes.

From an investment standpoint, the old adage to buy when there is fear in the streets is a good one and while not necessarily a perfect timing mechanism, it does remind us that by the time the world has realized markets and investment portfolios are falling, there is a time when it’s perhaps too early to buy (deploy cash if we have it) and yet too late to sell. We must remember that selling a stock essentially should be done in the expectation that we’re going to lose if we keep holding it. If we sell a stock just because it has already fallen, at which point it then immediately rallies and goes back upwards, we’re not doing ourselves any favours.

Despite what you may otherwise imagine, so far, 2026 is setting up to be another promising start to what is the fourth year of this ongoing bull market, post the 2021/2022 bear market, which was ending as we arrived at Raymond James. That said, I’m extremely pleased with our #AllINsync pool, and we just finished at a new ALL-TIME high of $12.7044/unit as of Tuesday, April 14th, 2026. More on this below!

Big Shifts Underway Though

For many years, I’ve been using the U.S. stock market (i.e., S&P 500) as a comparison when comparing charts/sectors/markets to gain perspective as to the relative strength. The U.S. market has a heavy technology focus and is frankly huge compared to most other markets… did you know that the top 51 companies in the U.S are larger than the biggest Canadian company (i.e., Royal Bank!?!?). Amazing, wouldn’t you agree? It helps to be mindful of these facts and characteristics. We have a large geography in this country but admittedly we have managed to post the absolute worst performance in the past 10 years on an economic growth per person basis. Ultimately, whether you’re retired or not, most agree that we’d want our country to succeed, and to continue to offer opportunities for our kids, (y)our grandkids, our neighbours and so forth.

I can assure you there are many tactics used by our current government (and our governments of years past) that are smoke screens to hide our reality. A federal politician just tried to suggest that a graduate from the University of Waterloo (this was just the example, but you can extrapolate the thinking) who decides to go and take a job at Microsoft in the U.S. should pay a $500,000 penalty to compensate the Canadian tax system for the brain drain, or loss via subsidized post-secondary education. Where do you stand on this? The real issue, as I just pointed out is that we don’t have the kinds of opportunities to offer what other countries can and our expensive tax regime only compounds the problem. Our government has now (on multiple occasions) taken a company to court to force them to stay and operate in Canada so they don’t take the jobs with them after making a business decision to leave. How would anyone feel if they were forced to only be friends with this person or that person, or forced to not travel outside of their city, or forced to work in a certain profession, or forced to give up their online privacy or spending data?

Commodities are back rising and if you’re only willing to assume the U.S. & Israel starting war with Iran is the reason, fine, but know that it’s not true. Even if the government were to meet its goal of 2% inflation, it would mean the value of our money erodes by 2% every year that goes by. The money we earn, the money we save, the money we invest and so forth. It’s how the system is built, but I digress…

AllINsync (RJI237)

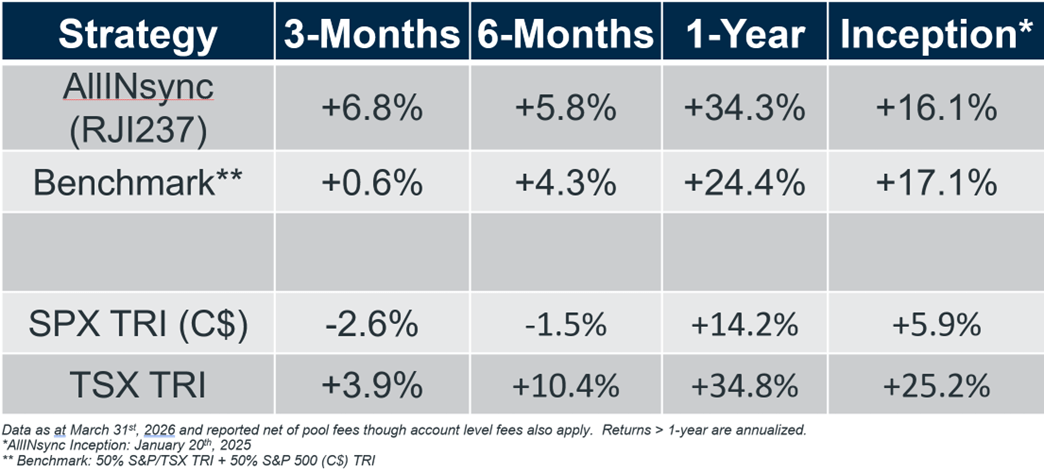

When we all contributed stocks, ETFs and cash to the AllINsync launch last spring, we had almost 130(!) different securities in there. It’s fair to say, the pool incepted with me knowing that there was going to be some work involved to mold it and shape it into what I envisioned, which was the all-encompassing product of our investment process that has been built over many years. Unlike the old days, where adapting to different markets was more challenging, given we had different models like “Equity INtrend” and “ETF 6/16” and “INvertigo”, AllINsync was going to bring together the ability to offer access to all the investment processes together, blended appropriately and proportionately to stay “Financially INsync” with changing global investment climates. And I think we’ve been doing just that! While the early rebalancing was underway, we were then thrown into further disarray as the markets turned nasty in February & March, 2025 (tariff tantrum/Liberation Day leadup) but we’ve emerged with a strong hand as I see it. If we’re critical, we can suggest that the inception returns since the January 20th, 2025 launch didn’t quite outperform, but if we dig deeper, we can see the promise that AllINsync offers. Remember, for 14+ years, the U.S. stock market was THE place to be (not Canadian stocks!) but that changed in late ’24, but really early ’25, and so on the one hand, our returns vs. the U.S. market (where we had most of our equity for years, and also at the inception date) have been excellent, of course I can smile if you say you’d have desired the stronger Canadian market in the past 16-months (can’t we always have the best of the best!?).

But one needs to know how to interpret data, to gain sharper insights. Look at the returns in the past 12-months because since March 31st, 2025, the market fell harshly into the lows on April 8th) – we’ve done really well and to the recent March 31st, 2026 quarter end, we have a +34.3% gain. We significantly outperformed the U.S. market, and also beat our 50/50 benchmark (a blend we have used with clients for longer than I can remember) by a wide margin (~+10%). At times, hearing some criticism the odd year in hindsight, i.e., why wouldn’t we compare to 100% U.S., my answer was always the same, cause they’re different markets and things change and we want to be prudent. And disciplined. Those of you that were clients in the mid 2000’s, might remember the days of Canadian stocks, particularly commodities and emerging markets soaring vs. the U.S. But after 14-years of relative downtrends, I can understand those memories faded (me too!). Either way, I digress (again)…

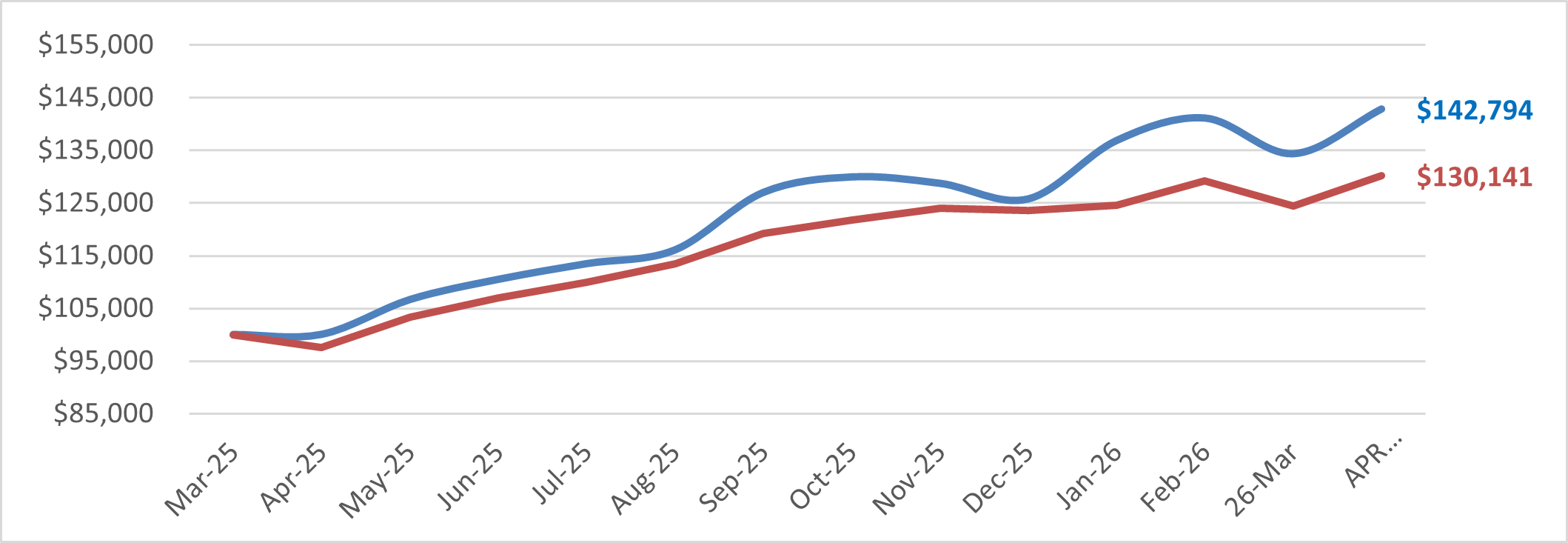

Here’s a chart of AllINsync vs. our 50/50 benchmark since March 31st, 2025 to the most current NAV (April 14th, 2026). The blue line is AllINsync vs. the 50/50 benchmark is red.

Source: Croesus/SSSG

Also here is the table of returns to the recent March 31st, 2026 quarter end. The past quarter, AllINsync returned +6.8% vs. only +0.6% for the benchmark (and you can see the U.S. market fell).

Tax Time

Some of you have noticed the new ease of tax filing requirements with the T3 for AllINsync (and less overall activity on the gain/loss statements!), but there were some changes you won’t have likely noticed. While there was no actual distribution of cash/units from AllINsync in 2025, it did produce a year-end phantom distribution (where the income was spit out on the T3 that you all received) and that in itself, caused an adjustment of the book value in your account (serving to reduce future capital gains). For example, if you had a taxable account and a $100,000 cost base of units purchased at $10 when the fund incepted, your account now shows a cost base of $103,260 ($10.326/unit) making it look like the difference between the market value and your actual purchase price is less than it actually is (understating your gain). Most of you are yawning (I understand!). Ask me a question if you want to better wrap your head around it. Bottom line – it’s much easier to file taxes now and it will be even easier in 2026 (with pool funding in the past).

Our Strategy & Our Allocation

While I can understand the potential confusion if I told you we currently have more exposure to the U.S. market vs. Canada, despite all the enthusiasm (and stronger returns) from the Canadian market, we must remember it’s a market of stocks. Different groups of stocks can drive the gains, and what’s most important is that we use relative strength to our advantage. Just because the broader U.S. market has been underperforming the Canadian market does not mean a U.S. stock we own is weaker (cause we like to pick strong ones!).

Our focus sectors right now are: industrials, energy, materials and technology (which recently re-emerged and frankly, these semiconductors, are tough to even attempt to criticize for losing relative strength). But the way, to adjust to changing conditions is to take risk off at market/sector/stock highs and add it back at lows, and that is how we operate. We have a stable of Canadian oriented ETFs offering a core, and some of the energy exposure that we have to complement our individual holdings that includes Cameco ($CCJ:US/$CCO:TSX) and Energy Fuels ($UUUU:US/$EFR:TSX). We also bought a couple of the Canadian banks, which are just been on a tear for some time (although still aren’t typically INsync Universe type stocks, with National Bank being the exception). We bought both CIBC (~5.2% position size) and National Bank (~5.1%) to own some of that strong industry group (i.e., financials on the whole aren’t a focus group, but the Canadian banks are a focus/leading industry group).

Our biggest position heading into quarter-end was Netflix, which after falling for 7-months started to show some technical signs, like “bullish divergences” and when a sign of demand came in late February, we joined in and bought shares. Using this type of buy methodology, we basically “buy for value” with a very tight stop (i.e., risk management is easy) and can risk a little to see if it ends up bottoming. And thus far, it seems like it did and we’re up ~+22.5% on our position.

“INvertigo” (the breakout buying methodology that was developed and defined by our team and incepted at the start of 2020), has come up short in the past year. Buying breakouts of more volatile growth stocks can be fun when they move explosively up, but tends to be a costly strategy when markets fall under pressure and volatility rises. On the one hand, I’m thankful that these days, when we see the challenges that breakouts are having, we can do little (or none) of such activity in the #AllINsync portfolio. Some of you have TFSAs which tend to be invested more aggressively that contain a proportion of INvertigo. Over the course of the last 3-6 months, each of these TFSAs also made a purchase of AllINsync itself, designed to anchor, and better stabilize/smooth out the expected returns. On the one hand, years ago, I would have tried to remain confident in the greater upside over time of INvertigo, but knowing it tends to suffer significantly over shorter time periods and it’s too volatile/uncertain to trust at times (too often!). Not only do very few of our clients have direct exposure to this model at this time, but the amount of exposure is quite small.

A Few Reminders & Closing Thoughts

What will the rest of 2026 bring? I don’t know and you know that I don’t like to make forecasts! But if I had to, I’d say we’re going to see more of the overall inflationary type environment that benefits commodities, Canada, emerging markets and so forth vis-à-vis the U.S., resembling the mid 2000’s period. We’ll see! And as usual, if and when the facts change (i.e., the market says differently), we’ll change right along with it! Happy Spring!

Thanks for reading this quarterly strategic review and your questions and/or comments are always welcome!

Sincerely,

David Cox, CFA, CMT, FMA, FCSI, BMath

Senior Portfolio Manager, Wealth Advisor

Raymond James Ltd.

Phone: 519.883.6031

Unit 1 – 595 Parkside Drive | Waterloo, ON | N2L 0C7

www.financiallyinsync.com

![]() @DavidCoxRJ

@DavidCoxRJ

Disclaimer: Information in this article is from sources believed to be reliable, however, we cannot represent that it is accurate or complete. It is provided as a general source of information and should not be considered personal investment advice or solicitation to buy or sell securities. The views are those of the author, Financially INsync Team, and not necessarily those of Raymond James Ltd. Investors considering any investment should consult with their Investment Advisor to ensure that it is suitable for the investor’s circumstances and risk tolerance before making any investment decision. Statistics, factual data and other information are from sources believed to be reliable, but accuracy cannot be guaranteed. It is furnished on the basis and understanding that Raymond James Ltd. is to be under no liability whatsoever in respect thereof. It is for information purposes only and is not to be construed as an offer or solicitation for the sale or purchase of securities.

Raymond James Ltd. is a Member Canadian Investor Protection Fund.

Raymond James (USA) Ltd. (RJLU) advisors may only conduct business with residents of the states and/or jurisdictions for which they are properly registered. Raymond James (USA) Ltd., member FINRA/SIPC.